AI in P&C Insurance Has Hit an Inflection Point

April 22, 2026

By Jim Bowers

Executives are shifting from experimentation to execution but scaling AI safely and effectively remains the biggest challenge.

Over the past year, one theme has come up in nearly every conversation we’ve had with carriers, TPAs, brokers, and self-insured organizations: AI is no longer theoretical.

Industry data supports this trajectory:

- 89% of insurers planned to increase investment in generative AI in 2025, and 92% already have dedicated budgets. 1

- 74% of firms identified it as a key area for underwriting and claims functions.

2

Executives aren’t asking what it is or whether it matters—they’re asking how to implement it, how to scale it, and how to do both without introducing risk.

What was experimentation a year ago is now execution. And the gap between pilots and real impact is where most organizations are stuck.

This blog is drawn from those conversations, combined with broader industry research and what we’re seeing across active implementations.

Where Carriers Are on the AI Journey

Executives describe their organizations as being somewhere between pilot mode and early scaling. Few have fully operationalized AI across business units, but nearly all have active initiatives underway.

- Exploration: Teams are experimenting with GenAI tools for summarization, document review, and internal knowledge search.

- Piloting: Carriers are testing underwriting assistants, claims agents, and customer service automation.

- Scaling: Governance frameworks, AI councils, and secure data platforms are being established.

- Operationalization: A small group of leaders are embedding AI into workflows and measuring ROI.

AI Adoption is not Equal

We are seeing the pace increase across the market, but there is a difference by size of organization and type of organization.

- TPAs are more focused on cost transfer to clients and having enough AI tools in place to use for marketing and client acquisition and retention.

- Carriers are in different stages of their journeys based on a few observed factors:

- Are they invested in legacy system upgrades to handle new technologies

- Have they taken any steps to consolidate and leverage disparate data assets

- Large and large-mid-sized carriers seem to be further along in terms of governance and regulatory considerations

- Larger carriers tend to have AI governance committees, policies, and established, but evolving protocols in place

- These carriers typically are more protective of their data assets

- They usually like to build when feasible vs. buy. This is particularly true the larger they get.

- Small and small-to-mid-sized carriers are often a few steps behind in their roadmap journey and sophistication but still are now more likely to be “buyers” and users of AI then in the past, when they were not early adopters or fast-followers.

- Brokers, PEOs, and Self-Insureds timelines and sophistication seem to match a similar pattern to carriers based on size of the organization.

Where AI Is Delivering Real Value

Claims: The Frontline of Impact

Claims lead the way.

- Predictive models improve triage and severity accuracy

- GenAI summarizes medical records and legal documents

- Automation reduces cycle times and leakage

What matters most: explainability. If adjusters trust it—and regulators understand it—it gets used.

Underwriting: From Data Overload to Decision Support

Underwriters don’t need more data; they need better decisions.

- AI extracts key insights from submissions and loss runs

- Models improve risk scoring and appetite alignment

- Assistants reduce manual work

The shift: AI isn’t replacing underwriters; it’s increasing their leverage.

Operations: The Fastest ROI

Operations teams are seeing immediate gains.

- Call summarization and real-time policy insights

- Automated workflows (policy changes, certificates)

- Faster, more accurate document processing

Result: Better customer experience with lower cost to serve.

What’s Slowing Scale

Despite momentum, four barriers keep coming up:

- Regulatory Pressure

Fairness, transparency, and consumer protection are non-negotiable. - Data Security

Carriers are drawing a hard line: no sensitive data in public models. - Governance Gaps

AI councils and controls are forming but still maturing. - Change Management

Adoption, not technology, is the bottleneck.

Build, Buy, or Partner? It’s All Three

Most carriers are landing on a hybrid model:

- Build core platforms and governance

- Buy specialized capabilities

- Partner to accelerate execution

The winning approach: Own the foundation. Leverage the ecosystem.

What Leaders Are Doing Differently

The organizations pulling ahead share three traits:

- They build governed AI platforms

Secure, reusable, and scalable across use cases - They focus on “lighthouse” wins

Targeted use cases with measurable ROI - They treat AI as a business capability

Not a side project or experiment

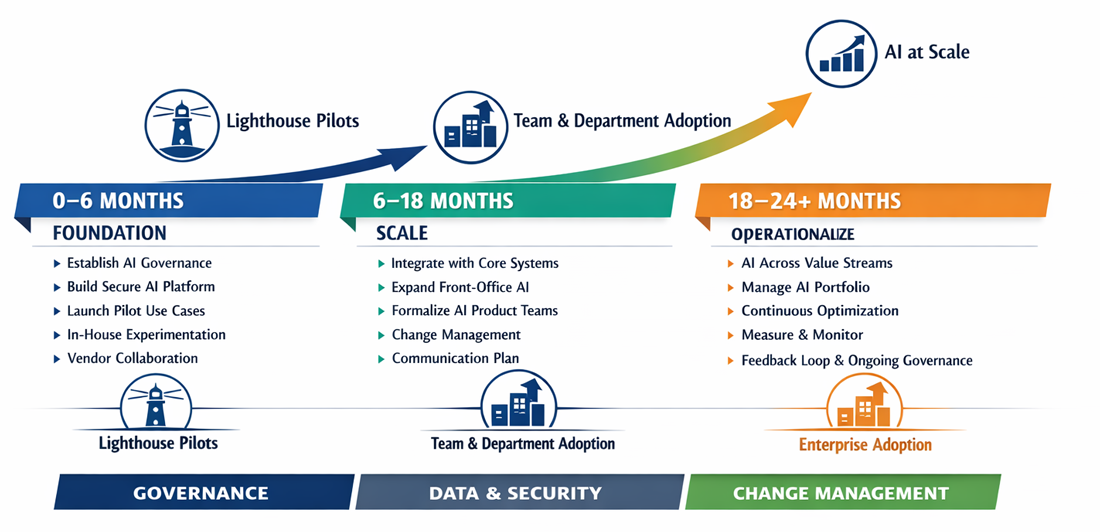

The Next 12–24 Months Will Separate Leaders

The roadmap is becoming clearer:

Now (0–6 months):

- Establish AI governance and responsible AI framework.

- Build secure enterprise AI platform.

- Launch 2–3 lighthouse use cases (claims, underwriting, operations).

Next (6–18 months):

- Integrate AI into core systems and workflows.

- Formalize AI product ownership and value tracking.

- Expand to front-office and agentic workflows.

Then (18+ months):

- Manage AI as a product portfolio.

- Embed AI into strategic planning and budgeting.

- Build continuous improvement and lifecycle management.

AI Implementation Roadmap for P&C Insurers

The Bottom Line

AI is no longer a future initiative. It’s a current competitive requirement.

Carriers aren’t deciding whether to adopt AI. They’re deciding how fast they can scale it without losing control.

The real risk isn’t moving too fast. It’s moving too slow while others figure it out.

1. SAAS, GenAI in Insurance: 3 key takeaways from a global industry survey, October 2024

2.

EY, How insurers are embracing customer-facing applications for GenAI, 2025 Survey Summary

Jim Bowers is the Principal Solutions Consultant for the Property & Casualty business at Gradient AI. He is a leader in the Workers’ Compensation insurance industry with more than 25 years of carrier experience across claims and underwriting.

Stay on top of AI trends by subscribing to Advanced Insights, the newsletter for strategies, ideas, and insights on AI insurance, delivered to your monthly inbox. Subscribe Now →